Advisor Blog

Negative Rates May Expand Market’s Multiple

The big news from economist Fritz Meyer's CE webinar on Advisors4Advisors on September 10, was his analysis of how negative rates in Germany are driving down bond yields in the U.S.

In recent weeks, Fritz has described a realignment in asset class valuations that makes it wise to expect lower returns on bonds permanently. To be clear, it’s reasonable to expect lower returns on bonds for the long run. Why? The main cause is changing national demographics of the world's major economies, a long-term fundamental factor driving the GDP growth rates and is an unsung competitive advantage for the U.S. versus other developed economies.

In the two-minute transcribed segment of his 75-minute presentation shown below, Fritz delves deeper into how negative rates are likely to impact U.S. financial assets and concludes it improves the stock market p/e ratio.

For financial advisors, tinkering with asset allocations of portfolios is not trivial. A revaluation of a core portfolio’s asset classes is not a trade; it’s not tactical. It’s a strategic asset allocation decision based on long-term economic fundamentals, and that's our approach in creating financial advisor content.

We put thought leadership on strategic financial planning and investment management into a proprietary advisor marketing dashboard,

Advisors often promise thought leadership of this kind but almost never deliver. Advisor Products content for advisor clients is unique in its fiduciary focus, as shown in the video below. It's an integrated marketing platform for financial advisor lead generation platform and client engagement.

Here below is the transcript Fritz Meyers about a long-term revaluation that may be under way. The slides and transcripts for Fritz's monthly webinars can be purchased for $50 a month.

If all you want is acces to Fritz's monthly webinars and CE credit for CFPs, it's only $10 a month .

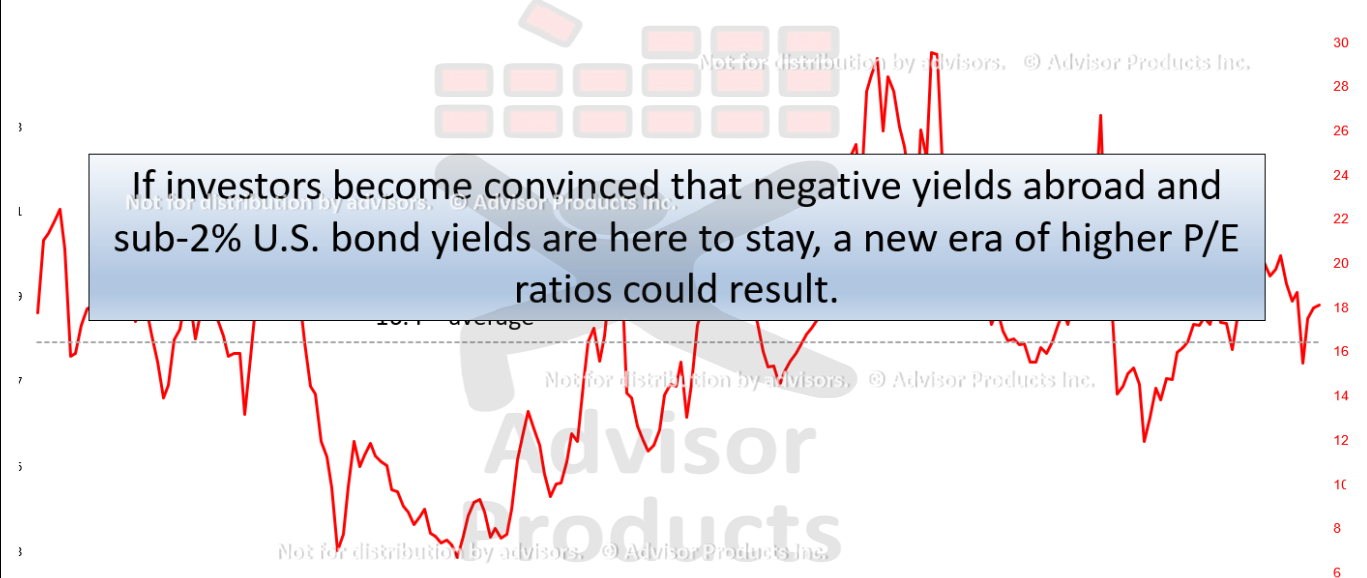

Now let’s address the market’s multiple explicitly, which is what you see in the top data series. And here, in the red data series, is the S&P 500 P/E ratio on trailing 12-month earnings, and it’s 18.1 times at present. It’s 16.3 times on 2020 operating earnings. By the way, in that calculation I’ve shifted forward from 2019 because we’re only less than four months away from the end of this year. So I’ve moved forward. But it’s 16.3 times on the 2020 earnings estimates.

Now here’s a major point that I wanted to make this month that I haven’t said before, so I included this box. If investors, in fact, become convinced that negative yields abroad and sub-2%U.S. bond yields are here to stay. I think it is entirely conceivable that we enter a new era of higher P/E ratios. And I don’t think that calculation is any secret to any of you because I think we all understand that the market’s P/E ratio is a direct function of inflation expectations and bond yields.

So if, in fact, investors come around to a notion … And this would be radically new, radically new, because we’ve never in the history of the world experienced negative bond yields, at least as far as I know. I’ve never read about any instance in which you have to pay the bank to hold your money or you have to pay a bondholder to hold your money. And yet, that’s the world today. Now, is this a transient phenomenon? Absolutely not. I don’t think it is. I don’t think it is. I think this is a new world. None of us have ever seen this. Nobody has ever anticipated this. It has seemed inconceivable, and yet that is, I think, what we’re looking at.

And my point with respect to market valuation is, to the extent investors start to internalize this … And they haven’t done this yet. This is brand-new thinking. This is cutting-edge. You are witnessing [laughs] a once in all-time history shift, possibly, in sentiment, suggesting that if bond yields are negative, then the only game in town increasingly becomes common stocks and yield on common stocks. Today’s dividend yield on the S&P 500 is about 1.9. And a bond is 1 and a half percent. And the bond could actually go lower. It could go lower. So my point is to suggest that, first of all, 18.1 times trailing earnings is right in line with the historic norm for a low-inflation environment. But secondly and more importantly, to the extent that new attitudes take hold with respect to the direction for bond yields longer-term, P/E ratios could conceivably find new higher plateau sustainable levels. It only makes sense. It only makes sense because of the relative attraction of common stocks versus fixed income. Hope everybody understands that because I think it’s such a significant point.

Related Posts

Archive

Questions?

How and why does the Advisor Products system work?

In today’s times, when consumers have become more demanding and tech-savvy, financial advisors must use content marketing to attract, inspire, engage, and convert their prospective customers.

A good content strategy is focused on developing and distributing consistent, valuable content to engage and retain prospective customers and target audience, via your website. Our content library provides financial advisors with fresh, high-quality financial content that is updated regularly, improving SEO along the way. And our automated e-newsletter and social media tools allow advisors to reach out to clients and prospects in an easy-to-use manner, providing frequent touch points for optimal brand building.

- Differentiate you from competitors

- Expose clients and prospects to your brand message more frequently

- Build an ongoing relationship with customers

- Increase your follows and fans on social media

- Drive more prospects to your website

- Help convert prospects into leads

- Increase number of pages indexed in Google

What products and services do you offer?

Can I buy services if my website is not hosted with you?

What can I expect during the onboarding process?

What if I have questions after my website is built?

Seeing is Believing.

See how easy it is to get started with our all-in-one digital marketing platform that drives leads, encourages referrals and increases client engagement.

SCHEDULE A DEMO

MARKETING TOOLS

LEARN MORE

RESOURCES

LATEST ARTICLES

Bank instability in March added a new risk an outlook already clouded by inflation and monetary policy problems hobbling the post-pandemic recovery. The bank runs came on top of the inflation crisis caused since the pandemic of April 2020 and March 2...

March 15 was one of the most pivotal days of the past 50 years, and financial advisors played a crucial role in getting the facts out about the banking panic to their clients and community. Trouble is, your messaging must be:as timely as WSJ, NYT, CN...

WEEKLY FINANCIAL MARKETING VIDEO

Watch The Video

Advisor Websites and More

Advisor Products delivers high-quality, FINRA approved financial news articles and branded weekly financial videos published automatically to your financial advisor website. We also offer marketing tools like our easy-to-use financial blog, automated financial enewsletters, social media marketing tools to help financial advisors disseminate content quickly and easily.

Advisor Products delivers high-quality, FINRA approved financial news articles and branded weekly financial videos published automatically to your financial advisor website. We also offer marketing tools like our easy-to-use financial blog, automated financial enewsletters, social media marketing tools to help financial advisors disseminate content quickly and easily.

By using Advisor Products you agree to our use of cookies to enhance your experience I understand