Advisor Blog

Lifeboat Drill As A Titanic Metaphor For UHNWIs

.

.

A lifeboat drill is a vivid and timely metaphorical device for urging clients and prospects to action. The seven-question drill in this pre-written article for advisors, which will be FINRA-reviewed, comes in the eleventh year of the expansion, at a time when stocks are hovering near an all-time high.This brief article for advisor clients asks seven questions designed to quickly surface risks that can sink families financially when things suddenly go terribly wrong in the markets and in one’s personal or professional life.

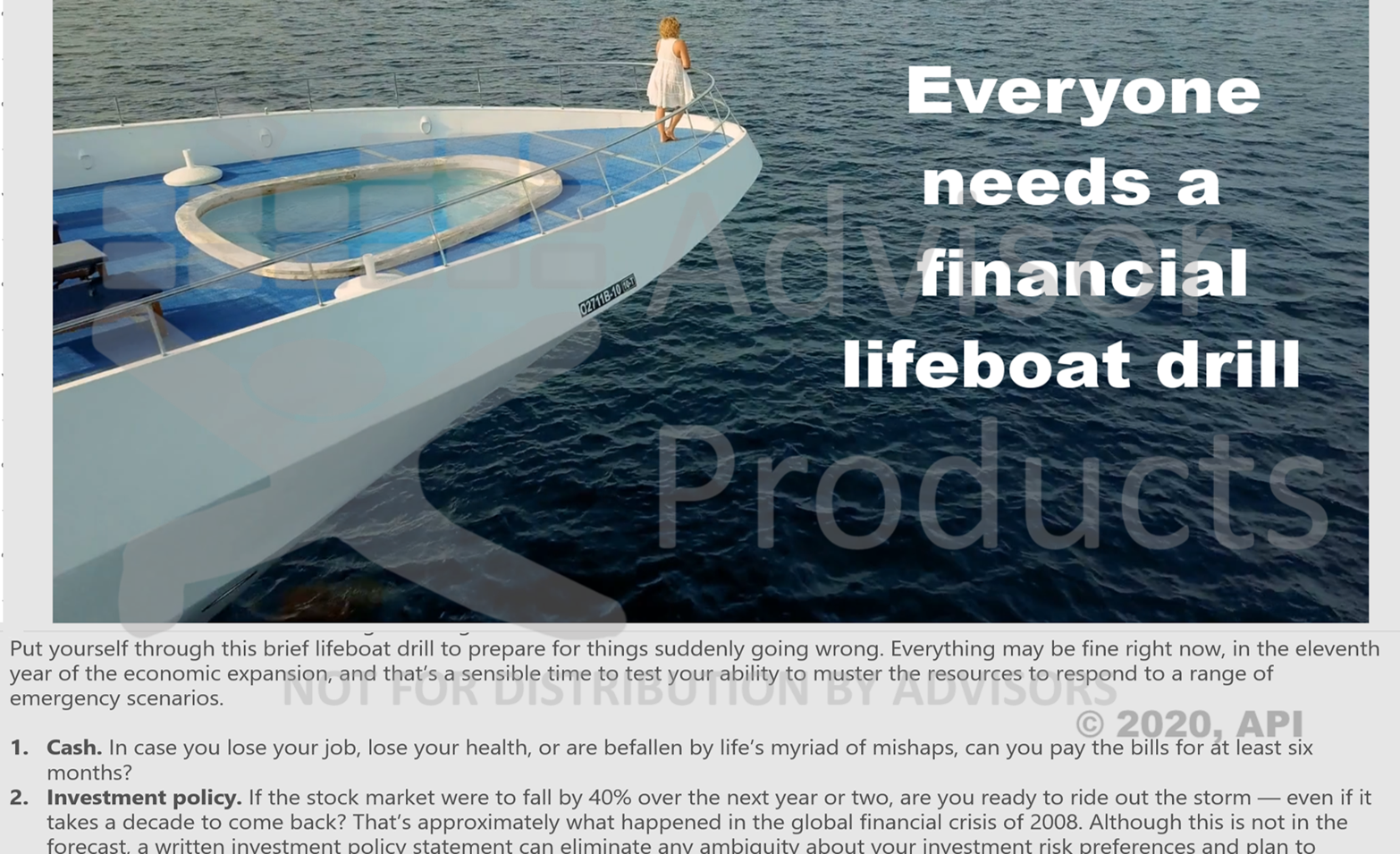

A lifeboat drill is not a new device for educating consumers about financial planning. It’s been illustrated in advisor marketing for decades, using an orange lifeboat or a lifesaver float to illustrate the concept. However, an elegantly dressed woman standing at the front of a luxury yacht better illustrates the point. The image conjures up the movie “Titanic,” to capture a scene inspired by the life of mass-affluent as well as ultra-high net-worth individuals.

That nuanced messaging is what separates Advisor Products educational marketing for CFA®,CFP®, CPA, and other fiduciaries from marketing registered reps, which serves up financial planning, tax and investment advice like junk food but wealth individuals who entrust you with managing their financial life can discern the difference between marketing puffery and thought leadership. Advisor Products content is based on accredited professional education classes. This article is inspired by a classes taught by tax guru, Bob Keebler's, 4.8-star rated class about 2020 planning techniques for advisor clients, which is avaiulable 24/7 for CE credit.

This article also meets an important Advisor Products test: It is not only for lead generation and building your practice, it is also relevant to your existing advisor clients. Writing from this perspective requires a thorough understanding of financial, tax, and investment planning as well as marketing and writing skills.

Marketing writers and consultants who do not have the requisite skills often deride “canned content” as ineffective but they simply don't know enough about tax, financial, and investment planning for affluent individuals to communciate with two advisor audiences in the same article, and they may just want to sell their services.

Creating FINRA-reviewed articles, videos, social media updates, and presentations for advisors that speak to these two distinct audiences requires years of experience in creating pre-written articles for CFP® and other professionals, in producing a news stream for wealthy individuals who value professional financial advice.

Advisor Products content is based on CE classes on A4A.TV and this lifeboat drill concept was inspired by CPA/PFS Bob Keebler's class, 2020 Financial & Tax Planning Practitioner Guidance, Here's the Q&A portion of that session, and a transcript of the Q&A. The concept for thisd class is loosely based last week's class led by Bob Keebler, "2020 Tax & Financial Planning Practitioner Guidance." Replay or read below the transcript of the 10-minute Q&A at the end of the session.

2020 Financial & Tax Planning Practitioner Guidance

(Below is a transcript of the last 10 minutes of a 60-minute, 1-credit continuing professional education class on Advisors4Advisors taught live for CPA-CPE on December 5, 2019 by Robert S. Keebler, CPA/PFS. CFP® and other professionals receive 24/7 CE credit by take the full class by joining A4A.TV for $120.)

Andrew Gluck: Questions? I had a couple of questions, too. But at the beginning, when you were talking about the possibility of tax change as soon as 2021, after the November 2020 election, I’m wondering, if the Senate ... Let’s say Trump does lose and the Senate doesn’t turn over.

Robert Keebler, CPA/PFS: Game over. Everything’s a standstill.

Andrew Gluck: OK, but does the likelihood of a tax increase rise in 2021 if that happens?

Robert Keebler, CPA/PFS: I don’t think so. I think the Senate would not allow that to happen.

Andrew Gluck: So, the possibility of a tax increase really rides on what happens with the Senate?

Robert Keebler, CPA/PFS: That’s right. Well, I mean, you’re assuming the president loses. Nobody knows what’s going to happen.

Andrew Gluck: Oh, of course. Of course. Right now, the polls are ... That’s what they’re saying, so that’s why I’m just trying to focus on that issue. Also, when you referenced Judge Ginsburg, is there a tax angle to it, or ... Because I was surprised that you brought that up and—

Robert Keebler, CPA/PFS: No, no, no. Here’s the important part. The Senate cannot get to SECURE. They’re saying they don’t have enough time. And if you want to see a very large use of the Senate’s time, it would be going through a confirmation hearing. Because look at what happened with Justice Kagan. Look at what happened with Justice Gorsuch. Kagan was more brutal than Gorsuch, but you can see we’ll have a period of time where the Senate is devoting their energies to vetting the next Supreme Court justice. That’s my only comment. There’s really not a tax angle to that. It’s more of like they’re not going to be able to get stuff done.

So, we know in January — it’s already been referred, pretty much — we’re going to have an impeachment hearing, which is going to take some time, right? And the issue, the way I understand it, is that all of the senators have to sit as a jury. So, if you’re in this hearing, you can’t get anything else done. And I suspect there won’t be ... I’ve done a lot of expert witness work. Most people aren’t going to have a lot of energy, after listening to that level of detail all day long, to do other things. They’re just going to be getting ready for the next day.

Andrew Gluck: That’s really amazing because you were, some months back, really sure that the SECURE Act was going to get done.

Robert Keebler, CPA/PFS: Yes. I’m embarrassed. Called it totally wrong.

Andrew Gluck: No. Well, we don’t know that yet. But your humility is appreciated. I have been sending you over those questions. We’ve got a lot of them. Do you want to just go through them?

Robert Keebler, CPA/PFS: Sure.

Andrew Gluck: Because you usually zip through them then.

Robert Keebler, CPA/PFS: OK, actually, I don’t see anything in my email from you yet.

Andrew Gluck: Oh, oh, oh. I’m sorry. They’re not in email, but I can put them in an email.

Robert Keebler, CPA/PFS: No, no, that’s OK. Let’s look.

Andrew Gluck: I’ve just been assigning—

Robert Keebler, CPA/PFS: Are they in the question pane?

Andrew Gluck: Yeah. Yeah, I’ve just been assigning them to you. But let me—

Robert Keebler, CPA/PFS: Let me try to open that up, Andy. Maybe just read a couple while I’m trying to open this up.

Andrew Gluck: Give me one second. I’m just going to email it to you so that I get that out of the way, and then I’ll read one.

Robert Keebler, CPA/PFS: OK. I have it open, Andy.

Andrew Gluck: Oh. Well, I’ll email them to you, but go ahead.

Robert Keebler, CPA/PFS: OK. Jason Hochstadt, writes, “Biden also wants to tax capital gains as ordinary income.” So, there we go.

Jeff says, “Don’t we need one common-law employee beyond a spouse to get ERISA protection?” Yes. I thought I said that, but if I didn’t articulate that right ... So, if it’s just husband and wife, you’re not going to get the ERISA protection you want. You’re stuck with state law. But if it’s husband and wife plus one other worker, then you’re going to get the ERISA protection you want.

OK, Kathleen writes, “Can the owner of an IRA have a CRT be the beneficiary of the RMD and take the income from the CRT?” No, but you can have your IRA paid to a CRT when you die.

“Are short-term losses against long-term gains still an issue in the lower tax brackets?” Probably not as much, Peter, because if you’re all at the zero rate, it doesn’t much matter. “When you’re planning for years beyond”—

Andrew Gluck: I’m sorry. What do you mean “still an issue”?

Robert Keebler, CPA/PFS: Oh, what Peter was talking about. My little chart with the four boxes of efficient/inefficient, that little box on the capital gain harvesting. Peter points out that if you’re making 30 grand, it’s not going to much matter because you’re all in a zero percent rate anyway.

“When you’re planning for years beyond 2025, do you assume continuing current tax rates and law or do you assume it will sunset?” Oh, I would assume we sunset.

Andrew Gluck: Great question. Read the question again, slowly, so that everybody—

Robert Keebler, CPA/PFS: OK. “When you’re planning for years beyond 2025, do you assume continuing current rates or do you assume a sunset?” I would assume a sunset. I just don’t see any way that we end up with something other than the sunset, because the tension between both political parties has been high for so long, I just don’t see any magic that’s going to happen to fix that.

Andrew Gluck: Yeah. Sam Fawas, thank you for that question. Sam Fawas. It’s probably Bawas. Bawas is probably it. I’m sorry.

Robert Keebler, CPA/PFS: Jeff writes, “Can you have a chance to talk a little bit about QBI, and how that may play into Roth conversion? And how about the Roth conversion amount may increase the QBI deduction?” OK, Jeff goes right to the deep end of the pool. OK, here’s the deal. So, you’re a barber. Your business income is 100 grand. But your taxable income, because you took a 24,000 standard deduction, is only 76,000 dollars. Your 199A deduction’s limited to 20 percent of 76,000 because it’s the lesser of your business income or your other income, your actual taxable income. If you did a 24,000-dollar Roth conversion, now your taxable income and your business income are pari passu. They’re the same. And now you get an additional 4800 dollars of 199A deduction. In other words, the essence is, if you’re in that situation, Jeff, your tax on your Roth conversion is reduced by 20 percent. Very, very good question.

OK, we only have a couple more. Peter writes, “Otherwise, the 3,000-dollar annual loss you can take against ordinary income has low future benefits.” Sure. That’s absolutely right. I mean, if you’re in the 10 or 12 percent bracket, that 3,000-dollar loss doesn’t mean much. But 12 percent of 3,000 dollars is 360 dollars you didn’t have. More importantly, maybe you can get somebody to clean up some of their portfolio, because we all like to live in this fantasy world that it’s not a real loss till you take it.

Andy, we’ve covered a lot of ground. We’ve actually gone over. It’s always an honor to be here with A4A. Back to you.

Andrew Gluck: You got a couple of more there I just forwarded over.

Robert Keebler, CPA/PFS: OK.

Andrew Gluck: And then, Nick is asking ... God, I don’t know why I ... I must be doing something wrong. The slides are available [laughs]. Because everybody asks this at every session, and I cover it at the beginning of every session. So, slides are available at AdvisorProducts dot com, and you could just chat us and we’ll send you the link. Ben, if you could chat out that link right now, that’ll be great. But they’re 50 dollars a month for the whole year. You just sign up and you get this whole database of all of Bob’s presentations. And we transcribe them. So, that’s how you do that. Nick, thank you for that question. And, Bob, do you see that? I think you got another question from Jason.

Robert Keebler, CPA/PFS: OK. Jason always asks the best questions. Should give him like a little medal or something, Andy.

Andrew Gluck: Jason Hogstadt, by the way, who does ask great questions.

Robert Keebler, CPA/PFS: “With respect to the Opportunity Zone funds, have you seen any offering liquidity to investors prior to year 10?” Not really.

And, yeah, “If everybody wants to sell, does that drive the price down?” You’re going to have to have restrictions. These agreements seem to have restrictions on how much you can sell, because, clearly, we all can’t bail at the same time.

And, “Aren’t the odds of capital gains being higher in 2026 great compared to now?” Yeah. Let’s say you had a million-dollar gain. If you just sold now, the worst the tax would be would be 238,000 dollars, OK? I think that’s right, 23.8, forgetting the state. So, it’s 238,000 dollars. But in the future, even though you’d — let me just do the math — even though you’d only pay tax on 85 percent of your gain, if you take 238 divided by 850, if we go up to a 28 percent rate, you’re in the same place and you’ve — this is interesting — and you’ve maybe just wasted all that time in that investment and you would’ve been better just to do something boring like buy a SPDR and not worry about it.

Now, the one thing about Opportunity Zone, though, is everybody’s forgetting. Let’s say I invest the million dollars in year one and I eventually have to pay tax on the million-dollar gain, minus the 15 percent basis I’m allowed. So, I eventually have to pay tax on 850. But let’s say that million-dollar investment 15 years from now has grown by 7 percent a year. Maybe it goes to 2 and a half million dollars, in round numbers. The gain from a million to 2 and a half million, under the law, is tax-free. So, what everybody’s missing ... Everybody gets all excited about the deferral and the 15 percent basis. That’s the bright, shiny object. What you should be focused on is that all the post-investment — the true gain on the investment, not the original gain you rolled in there but the true gain under the statute — is absolutely tax-free.

So, Jason, kind of think about that a little bit, too, because I think that’s what ... Especially me. I mean, I’ve been focused for months on the bright shiny object, and then I suddenly started really looking at this when I laid it out in an Excel spreadsheet for someone. And I kind of had an epiphany of what was really important here.

Andrew Gluck: OK. Yeah, Jason, thank you for that question again. And you see his response there in question, right, Bob?

Robert Keebler, CPA/PFS: Right. I mean, his last question is, “The opportunity zone developers are going to add the value right away. They might want to bail out.” I think the contracts will generally prevent them from bailing, but when we read these contracts, that’d be an important thing to look at. But if you’re going to put people in these sponsored opportunity zones, just really be careful that the company you’re dealing with is solid and that it’s just not a den of evil MBAs who expect to all make 3 million a year for doing very little. Because that’s my greatest fear on these things, is that all the people that work for the sponsors are extremely well-educated and probably earning very good salaries. And really, how much of the return are all those salaries going to absorb? Probably not a very nice thing to say, politically, but that’s what people like you guys and ladies have to be fearful of, is, “Who’s really getting the return on my client’s money, the sponsor or my client?”

Andrew Gluck: Great point. That’s really wonderful, because this area is attracting problems and I think that it’s up to the kind of professionals that attend these sessions to really kick the tires on these and watch out for package deals and sharks. And that’s the history of this kind of stuff. This always happens [laughs]. Every time, right? Bob, don’t you think? Whenever one of these tax deals comes along, there are always these characters that ... Now, you’re saying they’re sharp-elbowed MBAs. Who knows? But there’s so many greedy people out there, and this is a popular marketing idea, so I think your advice to really check the fundamentals is right on.

But I think I’ve got to find somebody that’s really kicking the tires on these things, and who has a good handle on the big picture on this. And they’re out there. And I will do that. I’ve got a new speaker coming on, on compliance, who’s really great for RIAs. And I’m working on some other speakers, and opportunity zones is definitely in my sights because it’s such an interesting area. It has so much potential. So, thank you for that, Jason and Bob. So, everybody, we went through pretty much all the questions, I think. I don’t think I missed any. But, wow, cool, we really got deep into it. So, thank you, everybody. Thank you, Bob. Great stuff.

Related Posts

Archive

Questions?

How and why does the Advisor Products system work?

In today’s times, when consumers have become more demanding and tech-savvy, financial advisors must use content marketing to attract, inspire, engage, and convert their prospective customers.

A good content strategy is focused on developing and distributing consistent, valuable content to engage and retain prospective customers and target audience, via your website. Our content library provides financial advisors with fresh, high-quality financial content that is updated regularly, improving SEO along the way. And our automated e-newsletter and social media tools allow advisors to reach out to clients and prospects in an easy-to-use manner, providing frequent touch points for optimal brand building.

- Differentiate you from competitors

- Expose clients and prospects to your brand message more frequently

- Build an ongoing relationship with customers

- Increase your follows and fans on social media

- Drive more prospects to your website

- Help convert prospects into leads

- Increase number of pages indexed in Google

What products and services do you offer?

Can I buy services if my website is not hosted with you?

What can I expect during the onboarding process?

What if I have questions after my website is built?

Seeing is Believing.

See how easy it is to get started with our all-in-one digital marketing platform that drives leads, encourages referrals and increases client engagement.

SCHEDULE A DEMO

MARKETING TOOLS

LEARN MORE

RESOURCES

LATEST ARTICLES

Bank instability in March added a new risk an outlook already clouded by inflation and monetary policy problems hobbling the post-pandemic recovery. The bank runs came on top of the inflation crisis caused since the pandemic of April 2020 and March 2...

March 15 was one of the most pivotal days of the past 50 years, and financial advisors played a crucial role in getting the facts out about the banking panic to their clients and community. Trouble is, your messaging must be:as timely as WSJ, NYT, CN...

WEEKLY FINANCIAL MARKETING VIDEO

Watch The Video

Advisor Websites and More

Advisor Products delivers high-quality, FINRA approved financial news articles and branded weekly financial videos published automatically to your financial advisor website. We also offer marketing tools like our easy-to-use financial blog, automated financial enewsletters, social media marketing tools to help financial advisors disseminate content quickly and easily.

Advisor Products delivers high-quality, FINRA approved financial news articles and branded weekly financial videos published automatically to your financial advisor website. We also offer marketing tools like our easy-to-use financial blog, automated financial enewsletters, social media marketing tools to help financial advisors disseminate content quickly and easily.

By using Advisor Products you agree to our use of cookies to enhance your experience I understand